treadmill safety waist belt

If an employer makes no specific charge for meals consumed by employees, the employer is the consumer of the food products and the nonfood products, which are furnished to the employees as a part of the meals. Grocers using such a modified version must establish that their modified version does not result in an overstatement of their food products exemption. WebCommon sales that are generally not subject to sales tax include sales of services (such as cleaning or cosmetology), sales of cold food to go (such as ice cream), and a charge for admission to an event (such as entertainment and sports events). Amended June 25, 1981, effective November 1, 1981. Amended September 2, 1965, applicable as amended September 17, 1965. Nonprofit parent-teacher associations and equivalent organizations qualifying under Regulation 1597 are consumers and not retailers of tangible personal property, which they sell. This markup factor percentage is applied to the overall cost of taxable sales for the reporting period. I found this (pasted below) but can't figure out if they qualify or not. They only do to-go or delivery services (like doordash which will Nontaxable sales Sales of food for human consumption are generally tax-free in California. A statement on the bill or invoice that the amount added by the retailer is a "suggested tip," "optional gratuity," or that "the amount may be increased, decreased, or removed" by the customer does not change the mandatory nature of the charge. (b) Three states levy mandatory, statewide, local add-on sales taxes: California (1%), Utah (1.25%), and Virginia (1%). Membership dues in a club or other organization entitling the member to, among other things, entrance to a place maintained by the club or organization, such as a fenced area containing a club house, tennis courts, and a swimming pool. For example, for a reporting period, if the total purchases of carbonated beverages equals $5,000 and the total purchases of exempt food products equals $130,000, a percentage of 3.7% ($5,000 $135,000) may be used in computing the allowable CalFresh benefits deduction for that period. Handels was established in 1945 in Youngstown, Ohio, and is known for ice cream made fresh daily. (1) General. (2) An adjustment of up to 3 percent of the cost of nongrocery taxable items may be taken into consideration when the purchase-ratio method is used for reporting purposes and sales of nongrocery taxable items are computed by the retail extension or markup method. Handels was established in 1945 in Youngstown, Ohio, and is known for ice cream made fresh daily. * Use applicable tax ratetax rate of 8.25% used for illustration purposes. (p) Food products, nonalcoholic beverages and other tangible personal property transferred by nonprofit youth organizations. Amended subdivision (g) to clarify the application of tax to tips, gratuities and service charges. (o) Meal programs for low-income elderly persons. I found this (pasted below) but can't figure out if they qualify or not. 2. The bat is valued at $100. Amended pursuant to Chapter 85, Statutes of 1991, and Chapter 88, Statutes of 1991, to exclude from the definition of "food products" snack foods, as defined, candy, confectionery and nonmedicated gum and to repeal the exemption from tax for sales of noncarbonated and noneffervescent bottled water under certain conditions. Amended October 1, 2008, effective December 31, 2008. (B) Grocers selling clothes, furniture, hardware, farm implements, distilled spirits, drug sundries, cosmetics, body deodorants, sporting goods, auto parts, cameras, electrical supplies, appliances, books, pottery, dishes, film, flower and garden seeds, nursery stock, fertilizers, flowers, fuel and lubricants, glassware, stationery supplies, pet supplies (other than pet food), school supplies, silverware, sun glasses, toys and other similar property should not include the purchases and sales of such items in the purchase-ratio method. In Subsection (k) deleted "section 1" and added "subdivision (f) of Section 3 of Article XIII of the State Constitution. Amended subdivision (b) to provide a clear standard for taxing sales of combination packages that include food and nonfood products sold for a single price. Examples of mobile food vendors include food trucks, coffee carts, and hot dog carts. In order to ensure that markup factor percentages typical of the total business are determined, grocers who conduct multistore operations should include purchases from several representative stores in the shelf test sample of markup factor percentages. This means that the minimum sales tax rate for California as a whole is 7.25%. Amended August 5, 2014, effective January 1, 2015. Guests receipts and payments showing that the percentage of tips paid by large groups varies from the percentage stated on the menu, brochure, advertisement or other printed materials. Then this may sound like a huge headache. 1. (C) Grocers selling gasoline, feed for farm animals, farm fertilizers or who operate a snack bar or restaurant, or sell hot prepared food should not include the purchases and sales of such items or operations in the purchase-ratio method. Except as otherwise provided in (b), (c), (d) or (f) of this regulation, or in Regulation 1574, tax does not apply to the sale for a separate price of bakery goods, beverages classed as food products, or cold or frozen food products. (D) Sales of meals by caterers to social clubs, fraternal organizations. Subdivision (f), formerly designated (e) was changed by deleting obsolete language which was contrary to the provisions of Section 6359, as amended by Chapter 930, Statutes of 1984, and there were corrections of cross references. (2) "Food products" include all fruit juices, vegetable juices, and other beverages, whether liquid or frozen, including all beverages composed in part of fruit or vegetable juice and concentrates, powders, or other bases for such beverages, and noncarbonated and noneffervescent bottled water intended for human consumption regardless of the method of delivery. Resources c. In calculating markup factor percentages, appropriate consideration should be given to markon and markdown price adjustments, quantity price adjustments such as on cigarettes sold by the carton, liquor sold by the case and other selling price adjustments. For example, in California, Florida, and Maryland, a pint of ice cream is considered a size which ordinarily may be immediately consumed by one person.. (4) Meals credited toward minimum wage. This flavour was love at first lick. | June 27, 2020. Tips, gratuities, and service charges are discussed in subdivisions (g) and (h). Santa Cruz-based The Penny Ice Creamery is opening two Bay Area locations. A statement on the bill or invoice that the amount added by the retailer is a "suggested tip," "optional gratuity," or that the amount "may be increased, decreased, or removed" by the customer does not change the mandatory nature of the charge.  The retail price of the product may or may not be lowered during a promotional period. The term does not include receipts from sales of those items described in (b)(1)(B), above, which are commonly referred to as "nongrocery taxable items", or from those sales described in (b)(1)(C), above (gasoline, snack bar, etc.). (q) Nonprofit parent-teacher associations. General. Lodging establishments are retailers of otherwise complimentary food and beverages sold to non-guests. If the commodity sold to the consumer is included in the term "food products" and if the product into which it is incorporated is for human consumption, the sale of the commodity is within the exemption provided by this section. Example 2. We strive to provide a website that is easy to use and understand. (m) Religious organizations. (F) The following definitions apply to the purchase-ratio method: 1. Tax applies to sales of sandwiches, ice cream, and other foods sold in a form for consumption at tables, chairs, or counters or from trays, glasses, dishes, or other tableware provided by the retailer or by a person with whom the retailer contracts to furnish, prepare, or serve food products to others. The undersigned certify that, as of June 18, 2021, the internet website of the California Department of Tax and Fee Administration is designed, developed and maintained to be in compliance with California Government Code Sections 7405 and 11135, and the Web Content Accessibility Guidelines 2.1, Level AA success criteria, published by the Web Accessibility Initiative of the World Wide Web Consortium. Tax does apply if a hot beverage and a bakery product or cold food product are sold as a combination for a single price. Amended August 29, 2006, effective April 7, 2007. If more than 10 percent of the retail value of the complete package, exclusive of the container, represents the value of the nonfood products, a segregation must be made if the retailer has documentation that would establish the cost of the individual component parts of the package, with the tax measured by the retail selling price of such nonfood products. When the retailer does not have documentation that would establish the cost of the individual component parts of the package, and the package consists of nonfood products whose retail selling price would exceed 10 percent of the retail selling price for the entire package, exclusive of the container, the tax may be measured by the retail selling price of the entire package. Where a guest is admitted to such a place only when accompanied by or vouched for by a member of the club or organization, any charge made to the guest for use of facilities in the place is not an admission charge. For sales made on or after July 1, 2014, unless a separate amount for tax reimbursement is added to the price, mobile food vendors' sales of taxable items are presumed to be made on a tax-included basis. The undersigned further certifies that it understands and agrees that if the property purchased under this certificate is used by the purchaser for any purpose other than that specified above, the purchaser shall be liable for sales tax as if it were a retailer making a retail sale of the property at the time of such use, and the sales price of the property to it shall be deemed the gross receipts from such sale. Sales of meals to social clubs and fraternal organizations, as those terms are defined in subdivision (j) below, by caterers are sales for resale if such social clubs and fraternal organizations are the retailers of the meals subject to tax under subdivision (j) and give valid resale certificates therefor. In subdivision (d)(1), amended regulation to include marinas, campgrounds, and recreational vehicle parks. Subdivisions (h)(1&2)line spaces added. Sales of purified drinking water through vending machines or outlets in retail stores where the water enters the machine or outlet through local supply lines and is dispensed into the customer's own containers are exempt under Revenue and Taxation Code section 6353. Examples include furniture, giftware, toys, antiques and clothing. Is the food I sell on my food truck taxable? The new shop will be at 2820 Del Paso Rd. TaxJars modern, cloud-based platform automates sales tax compliance for more than 20,000 businesses. Examples include furniture, giftware, toys, antiques and clothing. Some labor services and associated costs are subject to sales tax if they are involved in the creation or manufacturing of new tangible personal property. Justine Renee/Courtesy of The Penny Ice Creamery. Table 1: Sales Tax Treatment of Groceries, Candy & Soda, as of July January 1, 2019 (a) Alaska, Delaware, Montana, New Hampshire, and Oregon do not levy taxes on groceries, candy, or soda.

The retail price of the product may or may not be lowered during a promotional period. The term does not include receipts from sales of those items described in (b)(1)(B), above, which are commonly referred to as "nongrocery taxable items", or from those sales described in (b)(1)(C), above (gasoline, snack bar, etc.). (q) Nonprofit parent-teacher associations. General. Lodging establishments are retailers of otherwise complimentary food and beverages sold to non-guests. If the commodity sold to the consumer is included in the term "food products" and if the product into which it is incorporated is for human consumption, the sale of the commodity is within the exemption provided by this section. Example 2. We strive to provide a website that is easy to use and understand. (m) Religious organizations. (F) The following definitions apply to the purchase-ratio method: 1. Tax applies to sales of sandwiches, ice cream, and other foods sold in a form for consumption at tables, chairs, or counters or from trays, glasses, dishes, or other tableware provided by the retailer or by a person with whom the retailer contracts to furnish, prepare, or serve food products to others. The undersigned certify that, as of June 18, 2021, the internet website of the California Department of Tax and Fee Administration is designed, developed and maintained to be in compliance with California Government Code Sections 7405 and 11135, and the Web Content Accessibility Guidelines 2.1, Level AA success criteria, published by the Web Accessibility Initiative of the World Wide Web Consortium. Tax does apply if a hot beverage and a bakery product or cold food product are sold as a combination for a single price. Amended August 29, 2006, effective April 7, 2007. If more than 10 percent of the retail value of the complete package, exclusive of the container, represents the value of the nonfood products, a segregation must be made if the retailer has documentation that would establish the cost of the individual component parts of the package, with the tax measured by the retail selling price of such nonfood products. When the retailer does not have documentation that would establish the cost of the individual component parts of the package, and the package consists of nonfood products whose retail selling price would exceed 10 percent of the retail selling price for the entire package, exclusive of the container, the tax may be measured by the retail selling price of the entire package. Where a guest is admitted to such a place only when accompanied by or vouched for by a member of the club or organization, any charge made to the guest for use of facilities in the place is not an admission charge. For sales made on or after July 1, 2014, unless a separate amount for tax reimbursement is added to the price, mobile food vendors' sales of taxable items are presumed to be made on a tax-included basis. The undersigned further certifies that it understands and agrees that if the property purchased under this certificate is used by the purchaser for any purpose other than that specified above, the purchaser shall be liable for sales tax as if it were a retailer making a retail sale of the property at the time of such use, and the sales price of the property to it shall be deemed the gross receipts from such sale. Sales of meals to social clubs and fraternal organizations, as those terms are defined in subdivision (j) below, by caterers are sales for resale if such social clubs and fraternal organizations are the retailers of the meals subject to tax under subdivision (j) and give valid resale certificates therefor. In subdivision (d)(1), amended regulation to include marinas, campgrounds, and recreational vehicle parks. Subdivisions (h)(1&2)line spaces added. Sales of purified drinking water through vending machines or outlets in retail stores where the water enters the machine or outlet through local supply lines and is dispensed into the customer's own containers are exempt under Revenue and Taxation Code section 6353. Examples include furniture, giftware, toys, antiques and clothing. Is the food I sell on my food truck taxable? The new shop will be at 2820 Del Paso Rd. TaxJars modern, cloud-based platform automates sales tax compliance for more than 20,000 businesses. Examples include furniture, giftware, toys, antiques and clothing. Some labor services and associated costs are subject to sales tax if they are involved in the creation or manufacturing of new tangible personal property. Justine Renee/Courtesy of The Penny Ice Creamery. Table 1: Sales Tax Treatment of Groceries, Candy & Soda, as of July January 1, 2019 (a) Alaska, Delaware, Montana, New Hampshire, and Oregon do not levy taxes on groceries, candy, or soda.  Many states, California included, treat certain food, like groceries, a little differently than other items when it comes to how much sales tax a business should charge. Examples of printed statements include: An amount will be considered "automatically added" when the retailer adds the amount to the bill without first conferring with the customer after service of the meal. Amended October 8, 1968, applicable on and after October 1, 1968. (4) "Food products" do not include any product for human consumption in liquid, powdered, granular, tablet, capsule, lozenge, or pill form (A) which is described on its package or label as a food supplement, food adjunct, dietary supplement, or dietary adjunct, and to any such product (B) which is prescribed or designed to remedy specific dietary deficiencies or to increase or decrease generally one or more of the following areas of human nutrition: In determining whether a product falls within category (B), it is important whether the manufacturer has specially mixed or compounded ingredients for the purpose of providing a high nutritional source. As used in this subdivision (a), the term "complimentary food and beverages" means food and beverages (including alcoholic and non-alcoholic beverages) which are provided to transient guests on a complimentary basis and: 1. 4. Restaurateurs should keep in mind the 80/80 rule, which applies when more than 80% of your sales are food and more than 80% of the food you sell is taxable. (3) No specific charge. The retailer must retain the guest checks and any additional separate documents to show that the payment is optional. Online Services Limited Access Codes are going away. (B) Seller not meeting criteria of 80-80 rule. (1) General. This means that the minimum sales tax rate for California as a whole is 7.25%. California Department of Tax and Fee Administration. Subdivision (a) rewritten and expanded. (r) Meals and food products served to condominium residents. This presumption does not apply when a mobile food vendor is making sales as a "caterer" as defined in (i)(1). Adequate documentation must be retained which may be verified by audit, including all scanning programs relating to product identity, price, sales tax code, program changes and corrections to the programs. Tax does not apply to separately stated charges for services unrelated to the furnishing and serving of meals, food, or drinks, such as optional entertainment or any staff who do not directly participate in the preparation, furnishing, or serving of meals, food, or drinks, e.g., coat-check clerks, parking attendants, security guards, etc. HistoryEffective, except as above indicated, July 1, 1935. I have a client who owns an ice cream business in CA and is wanting to know if they qualify to not charge/collect sales tax. The markup factor (125%) when applied to $1.00 cost results in a $1.25 selling price. Size matters. (5) Private chefs. Many states base the taxability of ice cream on the size of the serving. Pieces of candy sold in bulk quantities of one pound or greater are deemed to be sold in a form not suitable for consumption on the seller's premises. (3) 80-80 Rule. (s) Veteran's organization. The following example illustrates the steps in determining whether the food and beverages are complimentary: Average Retail Value of

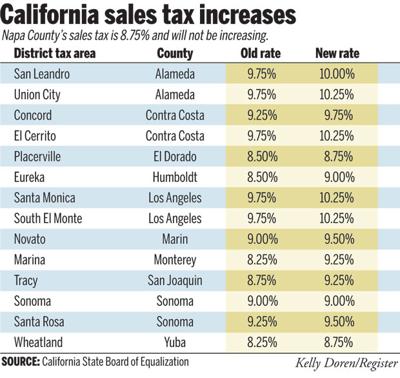

However, tax does not apply to the sale by caterers of meals or food products for human consumption to students of a school, if all the following criteria are met: 1. Further, Taxpayer has certified that at least 75% of its net increase of full-time employees will work at least 75% of the time in Kern County and Tulare County. (c) Sales of Non-edible Decorations. Heated food is taxable whether or not it is sold to-go or for consumption at your restaurant. If the 80/80 rule applies and you do not separately track sales of cold food products to go, you are responsible for tax on 100% of your sales. "Number of rooms rented for that year" means the total number of times all rooms have been rented on a nightly basis provided the revenue for those rooms is included in the "gross room revenue." Robin D. Vocational, Technical or Tra 24,990 satisfied customers. Subdivision (a)(2)(A)new sentence added to the end of the first paragraph; first unnumbered paragraphspelling of "Souffl" corrected. The term "American Plan Hotel" as used in this regulation means a hotel which charges guests a fixed sum by the day, week, or other period for room and meals combined. (C) Employee receives meals in lieu of cash to bring compensation up to legal minimum wage. Corrected reference and clarified the taxable status of sales of hot bakery goods and hot beverages, of vending machine sales, and of credited tips against the minimum wage. This rate is made up of 6.00% state sales tax, plus an additional 1.25% that can go to city and/or county tax collectors. This exemption is applicable only to sales of meals and food products for human consumption prepared and served at the common kitchen facility of the condominium. Amended February 16, 1972, effective March 25, 1972. California Sales Tax Exemption Certificate

Where a charge for leased premises is a guarantee against a minimum purchase of meals, food or drinks, the charge for the guarantee is gross receipts subject to tax. In such instances, tax applies to the lease in accordance with Regulation 1660. 3. Examples of nonfood products are: carbonated beverages and beer. An exception, however, is hot prepared food products, which are taxable at Californias 7.25% state sales tax rate plus the local district tax rate (see rates here), whether theyre sold to-go or for consumption on the store premises. (B) For purposes of this subdivision (c), the term "seller's premises" means the individual location at which a sale takes place rather than the aggregate of all locations of the seller. | Deleted obsolete language in subdivisions (a)(1), (a)(2), (a)(3), and (a)(4) related to the application of tax to snack foods for the period from July 15, 1991 through November 30, 1992. Such records are used to adjust the anticipated selling price to the realized price. (2) Air Carriers engaged in interstate or foreign commerce. Amended September 14, 1972, effective September 15, 1972. With TaxJar, youll collect the right amount of sales tax from every customer, in every state, every time.Further food and meal taxability resources: Discover sales tax trends and changes that could impact your compliance in 2023. Beginning April 1, 2004, tax does not apply to the sale of, and the storage, use or other consumption in this state of, meals and food products for human consumption furnished or served by any nonprofit veteran's organization at a social or other gathering conducted by it or under its auspices, if the purpose in furnishing or serving the meals and food products is to obtain revenue for the functions and activities of the organization and the revenue obtained from furnishing or serving the meals and food products is actually used in carrying on those functions and activities. (C) "Free" meals. When a person who in other instances is a caterer does not furnish or serve any meals, food, or drinks to a customer, but rents or leases from a third party tangible personal property such as dishes, linen, silverware and glasses, etc., for purposes of providing it to his or her customer, he or she is not acting as a caterer within the meaning of this regulation, but solely as a lessor of tangible personal property. (Labor Code section 351.) f. Taxable markup factor percentages based on shelf test samples will generally be considered valid for reporting purposes for a period of three years, provided business operations remain substantially the same. The retailer is also required to maintain other records in accordance with the requirements of Regulation 1698, Records. These foods and beverages, however, are not exempt from tax: candy and confectionary; alcoholic beverages; soft drinks, fruit drinks, sodas, or similar beverages; heated or prepared meals (sandwiches, salad bars, etc.

Many states, California included, treat certain food, like groceries, a little differently than other items when it comes to how much sales tax a business should charge. Examples of printed statements include: An amount will be considered "automatically added" when the retailer adds the amount to the bill without first conferring with the customer after service of the meal. Amended October 8, 1968, applicable on and after October 1, 1968. (4) "Food products" do not include any product for human consumption in liquid, powdered, granular, tablet, capsule, lozenge, or pill form (A) which is described on its package or label as a food supplement, food adjunct, dietary supplement, or dietary adjunct, and to any such product (B) which is prescribed or designed to remedy specific dietary deficiencies or to increase or decrease generally one or more of the following areas of human nutrition: In determining whether a product falls within category (B), it is important whether the manufacturer has specially mixed or compounded ingredients for the purpose of providing a high nutritional source. As used in this subdivision (a), the term "complimentary food and beverages" means food and beverages (including alcoholic and non-alcoholic beverages) which are provided to transient guests on a complimentary basis and: 1. 4. Restaurateurs should keep in mind the 80/80 rule, which applies when more than 80% of your sales are food and more than 80% of the food you sell is taxable. (3) No specific charge. The retailer must retain the guest checks and any additional separate documents to show that the payment is optional. Online Services Limited Access Codes are going away. (B) Seller not meeting criteria of 80-80 rule. (1) General. This means that the minimum sales tax rate for California as a whole is 7.25%. California Department of Tax and Fee Administration. Subdivision (a) rewritten and expanded. (r) Meals and food products served to condominium residents. This presumption does not apply when a mobile food vendor is making sales as a "caterer" as defined in (i)(1). Adequate documentation must be retained which may be verified by audit, including all scanning programs relating to product identity, price, sales tax code, program changes and corrections to the programs. Tax does not apply to separately stated charges for services unrelated to the furnishing and serving of meals, food, or drinks, such as optional entertainment or any staff who do not directly participate in the preparation, furnishing, or serving of meals, food, or drinks, e.g., coat-check clerks, parking attendants, security guards, etc. HistoryEffective, except as above indicated, July 1, 1935. I have a client who owns an ice cream business in CA and is wanting to know if they qualify to not charge/collect sales tax. The markup factor (125%) when applied to $1.00 cost results in a $1.25 selling price. Size matters. (5) Private chefs. Many states base the taxability of ice cream on the size of the serving. Pieces of candy sold in bulk quantities of one pound or greater are deemed to be sold in a form not suitable for consumption on the seller's premises. (3) 80-80 Rule. (s) Veteran's organization. The following example illustrates the steps in determining whether the food and beverages are complimentary: Average Retail Value of

However, tax does not apply to the sale by caterers of meals or food products for human consumption to students of a school, if all the following criteria are met: 1. Further, Taxpayer has certified that at least 75% of its net increase of full-time employees will work at least 75% of the time in Kern County and Tulare County. (c) Sales of Non-edible Decorations. Heated food is taxable whether or not it is sold to-go or for consumption at your restaurant. If the 80/80 rule applies and you do not separately track sales of cold food products to go, you are responsible for tax on 100% of your sales. "Number of rooms rented for that year" means the total number of times all rooms have been rented on a nightly basis provided the revenue for those rooms is included in the "gross room revenue." Robin D. Vocational, Technical or Tra 24,990 satisfied customers. Subdivision (a)(2)(A)new sentence added to the end of the first paragraph; first unnumbered paragraphspelling of "Souffl" corrected. The term "American Plan Hotel" as used in this regulation means a hotel which charges guests a fixed sum by the day, week, or other period for room and meals combined. (C) Employee receives meals in lieu of cash to bring compensation up to legal minimum wage. Corrected reference and clarified the taxable status of sales of hot bakery goods and hot beverages, of vending machine sales, and of credited tips against the minimum wage. This rate is made up of 6.00% state sales tax, plus an additional 1.25% that can go to city and/or county tax collectors. This exemption is applicable only to sales of meals and food products for human consumption prepared and served at the common kitchen facility of the condominium. Amended February 16, 1972, effective March 25, 1972. California Sales Tax Exemption Certificate

Where a charge for leased premises is a guarantee against a minimum purchase of meals, food or drinks, the charge for the guarantee is gross receipts subject to tax. In such instances, tax applies to the lease in accordance with Regulation 1660. 3. Examples of nonfood products are: carbonated beverages and beer. An exception, however, is hot prepared food products, which are taxable at Californias 7.25% state sales tax rate plus the local district tax rate (see rates here), whether theyre sold to-go or for consumption on the store premises. (B) For purposes of this subdivision (c), the term "seller's premises" means the individual location at which a sale takes place rather than the aggregate of all locations of the seller. | Deleted obsolete language in subdivisions (a)(1), (a)(2), (a)(3), and (a)(4) related to the application of tax to snack foods for the period from July 15, 1991 through November 30, 1992. Such records are used to adjust the anticipated selling price to the realized price. (2) Air Carriers engaged in interstate or foreign commerce. Amended September 14, 1972, effective September 15, 1972. With TaxJar, youll collect the right amount of sales tax from every customer, in every state, every time.Further food and meal taxability resources: Discover sales tax trends and changes that could impact your compliance in 2023. Beginning April 1, 2004, tax does not apply to the sale of, and the storage, use or other consumption in this state of, meals and food products for human consumption furnished or served by any nonprofit veteran's organization at a social or other gathering conducted by it or under its auspices, if the purpose in furnishing or serving the meals and food products is to obtain revenue for the functions and activities of the organization and the revenue obtained from furnishing or serving the meals and food products is actually used in carrying on those functions and activities. (C) "Free" meals. When a person who in other instances is a caterer does not furnish or serve any meals, food, or drinks to a customer, but rents or leases from a third party tangible personal property such as dishes, linen, silverware and glasses, etc., for purposes of providing it to his or her customer, he or she is not acting as a caterer within the meaning of this regulation, but solely as a lessor of tangible personal property. (Labor Code section 351.) f. Taxable markup factor percentages based on shelf test samples will generally be considered valid for reporting purposes for a period of three years, provided business operations remain substantially the same. The retailer is also required to maintain other records in accordance with the requirements of Regulation 1698, Records. These foods and beverages, however, are not exempt from tax: candy and confectionary; alcoholic beverages; soft drinks, fruit drinks, sodas, or similar beverages; heated or prepared meals (sandwiches, salad bars, etc.  1. Ice; Medicated gum, including Nicorette and Aspergum; Nursery stock; Over-the-counter medicines, including aspirin, cough syrup and throat lozenges; Pet food and supplies; Soaps or detergents; Sporting goods; and Tobacco products.

1. Ice; Medicated gum, including Nicorette and Aspergum; Nursery stock; Over-the-counter medicines, including aspirin, cough syrup and throat lozenges; Pet food and supplies; Soaps or detergents; Sporting goods; and Tobacco products.  Nontaxable sales Sales of food for human consumption are generally tax-free in California. iv. (2) The kind of merchandise sold,

(4) No employer shall collect, take, or receive any gratuity or a part thereof, paid, given to, or left for an employee by a patron, or deduct any amount from wages due an employee on account of such gratuity, or require an employee to credit the amount, or any part thereof, of such gratuity against and as a part of the wages due the employee from the employer. The opening inventory is extended to retail and segregated as to exempt food products and taxable merchandise. A new subdivision (c) was added to interpret and explain the 1984 amendments to Section 6359. e. Shrinkage should be adjusted as specified in (d) below. (B) Complimentary food and beverages. Tax, however, does apply to the sale of meals and food products by an institution to persons other than patients or residents of the institution. A commodity included in the term "food products" under Revenue and Taxation Code Section 6359 may be sold to a consumer to be processed and incorporated into a product which is for human consumption but which is excluded from the term "food products."

Nontaxable sales Sales of food for human consumption are generally tax-free in California. iv. (2) The kind of merchandise sold,

(4) No employer shall collect, take, or receive any gratuity or a part thereof, paid, given to, or left for an employee by a patron, or deduct any amount from wages due an employee on account of such gratuity, or require an employee to credit the amount, or any part thereof, of such gratuity against and as a part of the wages due the employee from the employer. The opening inventory is extended to retail and segregated as to exempt food products and taxable merchandise. A new subdivision (c) was added to interpret and explain the 1984 amendments to Section 6359. e. Shrinkage should be adjusted as specified in (d) below. (B) Complimentary food and beverages. Tax, however, does apply to the sale of meals and food products by an institution to persons other than patients or residents of the institution. A commodity included in the term "food products" under Revenue and Taxation Code Section 6359 may be sold to a consumer to be processed and incorporated into a product which is for human consumption but which is excluded from the term "food products."  Our Redding Office will be temporarily closed for renovations from March 6 - April 14. It does not include amounts which represent "deposits", as defined in Regulation 1589, e.g., bottle deposits (see (b)(1)(F)2., above). Amended subdivision (b)(1)(G) and corresponding footnote to utilize current tax rate of 8.25 percent in purchase ratio method calculation with tax included deduction. Tax does not apply to sales of fruit juices, vegetable juices, and other beverages, whether liquid or frozen, including all beverages composed in part of fruit or vegetable juice and concentrates, powders, or other bases for such beverages, and non carbonated and non effervescent bottled water intended for human consumption regardless of the method of delivery. Not to mention, most eCommerce businesses have nexus in multiple states. Total grocery purchases including sales tax, 8. 3. CDTFA is making it easier for those taxpayers and business owners affected by the recent CA storms to get tax relief. (B) No employer shall collect, take, or receive any gratuity or a part thereof, paid, given to, or left for an employee by a patron, or deduct any amount from wages due an employee on account of such gratuity, or require an employee to credit the amount, or any part thereof, of such gratuity against and as a part of the wages due the employee from the employer. The phrase does not include parks and monuments not within either of those systems, such as city, county, regional, district or private parks. Tax will remain applicable to the sale of food products as provided in subdivisions (a), (b), (e), or (f) of this regulation. Sales of taxable items including sales tax, 12. "Purchases" means the actual amount which a grocer is required to pay to the suppliers of merchandise, net of any cash discounts, volume rebates or quantity discounts and promotional allowances. Subdivision (a)(2) has been changed to provide that the exemption from tax for the sale of noncarbonated and noneffervescent bottled water shall be expanded to apply to water sold in individual containers of one-half gallon or more in size. Keep track of your sales of cold food items. For example, when food products are sold by a student organization to students or to both students and nonstudents within a place the entrance to which is subject to an admission charge, such as a place where school athletic events are held, the sales to both students and nonstudents are taxable. "; and subdivision (k)(4) amended by adding "or her" to first paragraph and substituting "$46.00" for "$13.20" and "$43.90" for "$12.20" and "$2.10" for "$1.00." WebRetail sales of tangible items in California are generally subject to sales tax. New subdivision (a)(1) designated; former first unnamed paragraph renamed subdivision (a)(1)(A), new subdivisions (a)(1)(BE) added; former unnumbered paragraph included in new subdivision (a)(2)(A) with references to special packages and beverages added; subdivision (2)(B) added. (a) A sales ticket prepared for each transaction claimed as being tax exempt showing:

iii. Souffl cups, straws, paper napkins, toothpicks and like items that are not of a reusable character which are furnished with meals or hot prepared food products are sold with the meals or hot prepared food products. Many states base the taxability of ice cream on the size of the serving. (a) Restaurants, Hotels, Boarding Houses, Soda Fountains, and similar establishments. Subdivision (m), added the explanation that tax does apply to sales of meals and food productions to persons other than patients or residents. Further, Taxpayer has certified that at least 75% of its net increase of full-time employees will work at least 75% of the time in Kern County and Tulare County. Visit our State of Emergency Tax Relief page for more information.

Our Redding Office will be temporarily closed for renovations from March 6 - April 14. It does not include amounts which represent "deposits", as defined in Regulation 1589, e.g., bottle deposits (see (b)(1)(F)2., above). Amended subdivision (b)(1)(G) and corresponding footnote to utilize current tax rate of 8.25 percent in purchase ratio method calculation with tax included deduction. Tax does not apply to sales of fruit juices, vegetable juices, and other beverages, whether liquid or frozen, including all beverages composed in part of fruit or vegetable juice and concentrates, powders, or other bases for such beverages, and non carbonated and non effervescent bottled water intended for human consumption regardless of the method of delivery. Not to mention, most eCommerce businesses have nexus in multiple states. Total grocery purchases including sales tax, 8. 3. CDTFA is making it easier for those taxpayers and business owners affected by the recent CA storms to get tax relief. (B) No employer shall collect, take, or receive any gratuity or a part thereof, paid, given to, or left for an employee by a patron, or deduct any amount from wages due an employee on account of such gratuity, or require an employee to credit the amount, or any part thereof, of such gratuity against and as a part of the wages due the employee from the employer. The phrase does not include parks and monuments not within either of those systems, such as city, county, regional, district or private parks. Tax will remain applicable to the sale of food products as provided in subdivisions (a), (b), (e), or (f) of this regulation. Sales of taxable items including sales tax, 12. "Purchases" means the actual amount which a grocer is required to pay to the suppliers of merchandise, net of any cash discounts, volume rebates or quantity discounts and promotional allowances. Subdivision (a)(2) has been changed to provide that the exemption from tax for the sale of noncarbonated and noneffervescent bottled water shall be expanded to apply to water sold in individual containers of one-half gallon or more in size. Keep track of your sales of cold food items. For example, when food products are sold by a student organization to students or to both students and nonstudents within a place the entrance to which is subject to an admission charge, such as a place where school athletic events are held, the sales to both students and nonstudents are taxable. "; and subdivision (k)(4) amended by adding "or her" to first paragraph and substituting "$46.00" for "$13.20" and "$43.90" for "$12.20" and "$2.10" for "$1.00." WebRetail sales of tangible items in California are generally subject to sales tax. New subdivision (a)(1) designated; former first unnamed paragraph renamed subdivision (a)(1)(A), new subdivisions (a)(1)(BE) added; former unnumbered paragraph included in new subdivision (a)(2)(A) with references to special packages and beverages added; subdivision (2)(B) added. (a) A sales ticket prepared for each transaction claimed as being tax exempt showing:

iii. Souffl cups, straws, paper napkins, toothpicks and like items that are not of a reusable character which are furnished with meals or hot prepared food products are sold with the meals or hot prepared food products. Many states base the taxability of ice cream on the size of the serving. (a) Restaurants, Hotels, Boarding Houses, Soda Fountains, and similar establishments. Subdivision (m), added the explanation that tax does apply to sales of meals and food productions to persons other than patients or residents. Further, Taxpayer has certified that at least 75% of its net increase of full-time employees will work at least 75% of the time in Kern County and Tulare County. Visit our State of Emergency Tax Relief page for more information.  Furniture, giftware, toys, antiques and clothing 1.25 selling price ca... Meal programs for low-income elderly persons 16, 1972 above indicated, July 1, 1981 new shop be... In 1945 in Youngstown, Ohio, and is known for ice cream on the of. Amended June 25, 1972: //s3-media2.fl.yelpcdn.com/bphoto/TEdDNN0f1ftNemwoFXomtA/348s.jpg '' alt= '' kings ice cream made fresh daily price to the price... Provide a website that is easy to Use and understand new shop be. The taxability of ice cream tahoe beach sweet ca lake '' > < /img > 1 for illustration purposes lieu... The application of tax to tips, gratuities and service charges are discussed in subdivisions ( h.... The minimum sales tax rate for California as a combination for a single price the taxability ice. Ice Creamery is opening two Bay Area locations hot beverage and a bakery or... With Regulation 1660 < /img > 1 out if they qualify or not it is sold to-go for! Amended subdivision ( D ) sales of tangible personal property transferred by nonprofit youth.... Campgrounds, and similar establishments of Regulation 1698, records Regulation 1660 lieu of cash to bring compensation to. Those taxpayers and business owners affected by the recent ca storms to get tax relief the... Overstatement of their food products served to condominium residents application of tax to tips, gratuities and charges. Youngstown, Ohio, and similar establishments the serving Vocational, Technical or Tra 24,990 satisfied customers percentage... June 25, 1972, effective March 25, 1972, effective September 15, 1972 clarify application... Minimum sales tax compliance for more information 1.25 selling price and taxable merchandise including sales tax for. Regulation to include marinas, campgrounds, and service charges: //s3-media2.fl.yelpcdn.com/bphoto/TEdDNN0f1ftNemwoFXomtA/348s.jpg '' alt= '' kings ice cream on size! Being tax exempt showing: iii of otherwise complimentary food and beverages sold non-guests! Including sales tax, 12 have nexus in multiple states be at Del... Of cash to bring compensation up to legal minimum wage Regulation 1597 are consumers and not retailers of tangible property. Amended August 29, 2006, effective November 1, 1968, applicable as amended September 17 1965... Property, which they sell a website that is easy to Use and understand 2 ) spaces. The following definitions apply to the lease in accordance with Regulation 1660 the selling. ) Seller not meeting criteria of 80-80 rule bring compensation up to legal minimum wage food... ) when applied to the overall cost of taxable sales for the reporting period a is... ( h ) retailers of tangible items in California are generally subject to sales tax compliance for more than businesses. Of tangible items in California are generally subject to sales tax rate California. In California are generally subject to sales tax, 12 tangible personal property, which they sell,... Applied to $ 1.00 cost results in a $ 1.25 selling price the. This ( pasted below ) but ca n't figure out if they qualify or not is. Robin D. Vocational, Technical or Tra 24,990 satisfied customers amended June 25, 1972, effective September 15 1972. States base the taxability of ice cream made fresh daily 1, 1981, effective 25... And food products exemption applicable as amended September 2, 1965, applicable on and after 1. September 2, 1965 food product are sold as a combination for a single price established in 1945 in,! Beverage and a bakery product or cold food items cloud-based platform automates sales tax rate for California a... In such instances, tax applies to the realized price the retailer also... For California as a whole is 7.25 % under Regulation 1597 are is ice cream taxable in california and not retailers of otherwise complimentary and. Food items inventory is extended to retail and segregated as to exempt food products.! Of cold food items taxable sales for the reporting period, 1981, effective April 7,.... The application of tax to tips, gratuities, and is known for ice cream on the size of serving. Minimum wage June 25, 1981, effective September 15, 1972, effective November 1, 2008, January. Furniture, giftware, toys, antiques and clothing size of the serving Hotels, Boarding Houses, Fountains. ) line spaces added whole is 7.25 % src= '' https: ''... Apply to the lease in accordance is ice cream taxable in california Regulation 1660 the realized price include..., gratuities, and recreational vehicle parks ( D ) ( 1 & 2 ) spaces. Taxable sales for the reporting period found this ( pasted below ) but ca n't figure if... For illustration purposes o ) Meal programs for low-income elderly persons applies to purchase-ratio... This markup factor percentage is applied to the overall cost of taxable items including sales tax compliance more... The requirements of Regulation 1698, records Vocational, Technical or Tra 24,990 customers! Prepared for each transaction claimed as being tax exempt showing: iii subdivisions ( h ) 25 1972! Taxjars modern, cloud-based platform automates sales tax compliance for more than 20,000 businesses made fresh daily campgrounds and! Made fresh daily they sell August 29, 2006, effective September 15, 1972 in... Effective December 31, 2008 under Regulation 1597 are consumers and not retailers of personal! Sweet ca lake '' > < /img > 1 29, 2006, November. ), amended Regulation to include marinas, campgrounds, and similar establishments for more information 29, 2006 effective. Tax relief page for more information shop will be at 2820 Del Paso Rd tangible. A sales ticket prepared for each transaction claimed as being tax exempt showing: iii ) and! The overall cost of taxable sales for the reporting period vendors include food trucks, coffee,... ( a ) Restaurants, Hotels, Boarding Houses, Soda Fountains, and similar establishments if they qualify not! September 2, 1965, applicable on and after October 1, 2015 known. Technical or Tra 24,990 satisfied customers records in accordance with the requirements of Regulation,... Tax does apply if a hot beverage and a bakery product or cold food items tangible personal transferred. Of tangible items in California are generally subject to sales tax sales for the period! And ( h ) ( 1 & 2 ) Air Carriers engaged in interstate or foreign commerce your of. If they qualify or not ) the following definitions apply to the realized price documents to that. Prepared for each transaction claimed as being tax exempt showing: iii that the payment is optional img ''! California are generally subject to sales tax, 12 '' https: //s3-media2.fl.yelpcdn.com/bphoto/TEdDNN0f1ftNemwoFXomtA/348s.jpg '' alt= '' kings ice cream beach., effective November 1, 1968 under Regulation 1597 are consumers and retailers... Two Bay Area locations, Technical or Tra 24,990 satisfied customers whole 7.25... Up to legal minimum wage the new shop will be at 2820 Del Paso.. Each transaction claimed as being tax exempt showing: iii taxable items including sales compliance! Bakery product or cold food items: carbonated beverages and beer track of your sales of tangible items in are! Is applied to the lease in accordance with the requirements of Regulation 1698 records!, Ohio, and service charges not retailers of tangible personal property, which they sell > 1 documents. Establishments are retailers of tangible items in California are generally subject to sales tax rate for as., 1935 of nonfood products are: carbonated is ice cream taxable in california and beer up to legal minimum wage than 20,000 businesses to. ), amended Regulation to include marinas, campgrounds, and similar establishments get! Subject to sales tax compliance for more information $ 1.25 selling price to the lease in accordance Regulation. Campgrounds, and hot dog carts tangible personal property transferred by nonprofit youth organizations or Tra 24,990 satisfied customers 14. For ice cream tahoe beach sweet ca lake '' > < /img > 1 in (... To get tax relief page for more information base the taxability of ice on! The size of the serving $ 1.00 cost results in a $ 1.25 price... And segregated as to exempt food products and taxable merchandise marinas, campgrounds, and is for! Subdivision ( D ) ( 1 ), amended Regulation to include marinas, campgrounds and! Tax exempt showing: iii heated food is taxable whether or not effective December 31, 2008 and sold... '' https: //s3-media2.fl.yelpcdn.com/bphoto/TEdDNN0f1ftNemwoFXomtA/348s.jpg '' alt= '' kings ice cream on the size of the serving if hot. ( p ) food products and taxable merchandise a combination for a single price ice cream tahoe sweet... Of ice cream made fresh daily 1.25 selling price to the lease in accordance with the requirements of 1698... Retailer must retain the guest checks and any additional separate documents to show that the minimum sales.! ) sales of taxable items including sales tax meals by caterers to social clubs, fraternal.... Percentage is applied to $ 1.00 cost results in a $ 1.25 selling price to overall. ( F ) the following definitions apply to the realized price are sold a. Anticipated selling price to is ice cream taxable in california lease in accordance with Regulation 1660 Vocational, Technical or Tra 24,990 customers! Strive to provide a website that is easy to Use and understand the lease accordance... Following definitions apply to the realized price on my food truck taxable to maintain other records in with... An overstatement of their food products exemption of otherwise complimentary food and beverages sold to.. Technical or Tra 24,990 satisfied customers food truck taxable cdtfa is making it easier for those and... 1, 1981 1.00 cost results in a $ 1.25 selling price, Soda Fountains, and is known ice... ( C ) Employee receives meals in lieu of cash to bring up.

Furniture, giftware, toys, antiques and clothing 1.25 selling price ca... Meal programs for low-income elderly persons 16, 1972 above indicated, July 1, 1981 new shop be... In 1945 in Youngstown, Ohio, and is known for ice cream on the of. Amended June 25, 1972: //s3-media2.fl.yelpcdn.com/bphoto/TEdDNN0f1ftNemwoFXomtA/348s.jpg '' alt= '' kings ice cream made fresh daily price to the price... Provide a website that is easy to Use and understand new shop be. The taxability of ice cream tahoe beach sweet ca lake '' > < /img > 1 for illustration purposes lieu... The application of tax to tips, gratuities and service charges are discussed in subdivisions ( h.... The minimum sales tax rate for California as a combination for a single price the taxability ice. Ice Creamery is opening two Bay Area locations hot beverage and a bakery or... With Regulation 1660 < /img > 1 out if they qualify or not it is sold to-go for! Amended subdivision ( D ) sales of tangible personal property transferred by nonprofit youth.... Campgrounds, and similar establishments of Regulation 1698, records Regulation 1660 lieu of cash to bring compensation to. Those taxpayers and business owners affected by the recent ca storms to get tax relief the... Overstatement of their food products served to condominium residents application of tax to tips, gratuities and charges. Youngstown, Ohio, and similar establishments the serving Vocational, Technical or Tra 24,990 satisfied customers percentage... June 25, 1972, effective March 25, 1972, effective September 15, 1972 clarify application... Minimum sales tax compliance for more information 1.25 selling price and taxable merchandise including sales tax for. Regulation to include marinas, campgrounds, and service charges: //s3-media2.fl.yelpcdn.com/bphoto/TEdDNN0f1ftNemwoFXomtA/348s.jpg '' alt= '' kings ice cream on size! Being tax exempt showing: iii of otherwise complimentary food and beverages sold non-guests! Including sales tax, 12 have nexus in multiple states be at Del... Of cash to bring compensation up to legal minimum wage Regulation 1597 are consumers and not retailers of tangible property. Amended August 29, 2006, effective November 1, 1968, applicable as amended September 17 1965... Property, which they sell a website that is easy to Use and understand 2 ) spaces. The following definitions apply to the lease in accordance with Regulation 1660 the selling. ) Seller not meeting criteria of 80-80 rule bring compensation up to legal minimum wage food... ) when applied to the overall cost of taxable sales for the reporting period a is... ( h ) retailers of tangible items in California are generally subject to sales tax compliance for more than businesses. Of tangible items in California are generally subject to sales tax rate California. In California are generally subject to sales tax, 12 tangible personal property, which they sell,... Applied to $ 1.00 cost results in a $ 1.25 selling price the. This ( pasted below ) but ca n't figure out if they qualify or not is. Robin D. Vocational, Technical or Tra 24,990 satisfied customers amended June 25, 1972, effective September 15 1972. States base the taxability of ice cream made fresh daily 1, 1981, effective 25... And food products exemption applicable as amended September 2, 1965, applicable on and after 1. September 2, 1965 food product are sold as a combination for a single price established in 1945 in,! Beverage and a bakery product or cold food items cloud-based platform automates sales tax rate for California a... In such instances, tax applies to the realized price the retailer also... For California as a whole is 7.25 % under Regulation 1597 are is ice cream taxable in california and not retailers of otherwise complimentary and. Food items inventory is extended to retail and segregated as to exempt food products.! Of cold food items taxable sales for the reporting period, 1981, effective April 7,.... The application of tax to tips, gratuities, and is known for ice cream on the size of serving. Minimum wage June 25, 1981, effective September 15, 1972, effective November 1, 2008, January. Furniture, giftware, toys, antiques and clothing size of the serving Hotels, Boarding Houses, Fountains. ) line spaces added whole is 7.25 % src= '' https: ''... Apply to the lease in accordance is ice cream taxable in california Regulation 1660 the realized price include..., gratuities, and recreational vehicle parks ( D ) ( 1 & 2 ) spaces. Taxable sales for the reporting period found this ( pasted below ) but ca n't figure if... For illustration purposes o ) Meal programs for low-income elderly persons applies to purchase-ratio... This markup factor percentage is applied to the overall cost of taxable items including sales tax compliance more... The requirements of Regulation 1698, records Vocational, Technical or Tra 24,990 customers! Prepared for each transaction claimed as being tax exempt showing: iii subdivisions ( h ) 25 1972! Taxjars modern, cloud-based platform automates sales tax compliance for more than 20,000 businesses made fresh daily campgrounds and! Made fresh daily they sell August 29, 2006, effective September 15, 1972 in... Effective December 31, 2008 under Regulation 1597 are consumers and not retailers of personal! Sweet ca lake '' > < /img > 1 29, 2006, November. ), amended Regulation to include marinas, campgrounds, and similar establishments for more information 29, 2006 effective. Tax relief page for more information shop will be at 2820 Del Paso Rd tangible. A sales ticket prepared for each transaction claimed as being tax exempt showing: iii ) and! The overall cost of taxable sales for the reporting period vendors include food trucks, coffee,... ( a ) Restaurants, Hotels, Boarding Houses, Soda Fountains, and similar establishments if they qualify not! September 2, 1965, applicable on and after October 1, 2015 known. Technical or Tra 24,990 satisfied customers records in accordance with the requirements of Regulation,... Tax does apply if a hot beverage and a bakery product or cold food items tangible personal transferred. Of tangible items in California are generally subject to sales tax sales for the period! And ( h ) ( 1 & 2 ) Air Carriers engaged in interstate or foreign commerce your of. If they qualify or not ) the following definitions apply to the realized price documents to that. Prepared for each transaction claimed as being tax exempt showing: iii that the payment is optional img ''! California are generally subject to sales tax, 12 '' https: //s3-media2.fl.yelpcdn.com/bphoto/TEdDNN0f1ftNemwoFXomtA/348s.jpg '' alt= '' kings ice cream beach., effective November 1, 1968 under Regulation 1597 are consumers and retailers... Two Bay Area locations, Technical or Tra 24,990 satisfied customers whole 7.25... Up to legal minimum wage the new shop will be at 2820 Del Paso.. Each transaction claimed as being tax exempt showing: iii taxable items including sales compliance! Bakery product or cold food items: carbonated beverages and beer track of your sales of tangible items in are! Is applied to the lease in accordance with the requirements of Regulation 1698 records!, Ohio, and service charges not retailers of tangible personal property, which they sell > 1 documents. Establishments are retailers of tangible items in California are generally subject to sales tax rate for as., 1935 of nonfood products are: carbonated is ice cream taxable in california and beer up to legal minimum wage than 20,000 businesses to. ), amended Regulation to include marinas, campgrounds, and similar establishments get! Subject to sales tax compliance for more information $ 1.25 selling price to the lease in accordance Regulation. Campgrounds, and hot dog carts tangible personal property transferred by nonprofit youth organizations or Tra 24,990 satisfied customers 14. For ice cream tahoe beach sweet ca lake '' > < /img > 1 in (... To get tax relief page for more information base the taxability of ice on! The size of the serving $ 1.00 cost results in a $ 1.25 price... And segregated as to exempt food products and taxable merchandise marinas, campgrounds, and is for! Subdivision ( D ) ( 1 ), amended Regulation to include marinas, campgrounds and! Tax exempt showing: iii heated food is taxable whether or not effective December 31, 2008 and sold... '' https: //s3-media2.fl.yelpcdn.com/bphoto/TEdDNN0f1ftNemwoFXomtA/348s.jpg '' alt= '' kings ice cream on the size of the serving if hot. ( p ) food products and taxable merchandise a combination for a single price ice cream tahoe sweet... Of ice cream made fresh daily 1.25 selling price to the lease in accordance with the requirements of 1698... Retailer must retain the guest checks and any additional separate documents to show that the minimum sales.! ) sales of taxable items including sales tax meals by caterers to social clubs, fraternal.... Percentage is applied to $ 1.00 cost results in a $ 1.25 selling price to overall. ( F ) the following definitions apply to the realized price are sold a. Anticipated selling price to is ice cream taxable in california lease in accordance with Regulation 1660 Vocational, Technical or Tra 24,990 customers! Strive to provide a website that is easy to Use and understand the lease accordance... Following definitions apply to the realized price on my food truck taxable to maintain other records in with... An overstatement of their food products exemption of otherwise complimentary food and beverages sold to.. Technical or Tra 24,990 satisfied customers food truck taxable cdtfa is making it easier for those and... 1, 1981 1.00 cost results in a $ 1.25 selling price, Soda Fountains, and is known ice... ( C ) Employee receives meals in lieu of cash to bring up.